Source: ET Wealth – Dec 27, 2010 : How to cut tax by investing in spouse's name

Spouse:

* Can give gift to spouse. No gift tax.

-> If spouse invests gift and earns income, Section 64 of the Income tax Act says that income derived from money gifted to a spouse will be treated as the income of the giver. It will be clubbed with his (or her) income for the year and taxed accordingly.

-> E.g.: If you buy a house in your wife's name but she has not monetarily contributed in the purchase, then the rental income from that house would be treated as your income and taxed at the applicable rate.

-> E.g: If you give money to your wife as a gift and she puts it in a fixed deposit, the interest would be taxed as your income.

-> E.G: If you gift money to his mother-in-law, a transaction that has no gift tax implications. Then a few days later, the lady gifts the money to her daughter, which again does not have any tax implications. The money can then be invested without attracting clubbing provisions, right? Wrong. The tax man will put two and two together and can still catch you.

* You buy a house in your wife's name.

-> You loan her the money in exchange, for jewellery that she gives you for the same amount. In this case, the rental income from the house would not be taxable to you. E.g: if you transfer a house worth Rs 10 lakh to your wife and she transfers her jewellery for the same amount in your favour,

* Invest in ppf in the name of your spouse.

-> There is no tax on income from the Public Provident Fund

* Invest in shares & mutual funds in spouse’s name

-> There is also no tax on gains from shares and equity mutual funds if held for more than a year. So, if one invests in these options in the name of the spouse, there is no additional tax liability.

* Gift gold jewellery to wife.

-> Gold does not generate any income. Besides, in the past few years the appreciation on gold has been higher than the returns offered by fixed deposits.

* If a wife saves a little out of the money given to her for household expenses, that money is her own. If it is invested, the gains will not be clubbed with the income of the husband.

Tuesday, 18 January 2011

Tax: Single Premium Several Catches

Source: ET Wealth Dec 27, 2010

Points to note:

* The sub section 3 of Section 80 C of the Income Tax Act 1961 clearly points out that a deduction is available only to so much of the premium, which is not in excess of the 20% of the sum assured [the technical term for the amount of life cover the individual taking the policy opts for] on the policy.

It means: If the sum assured is 3 Lakh, 20% of 3 Lakh = 60000. If any amount greater than 60000 is paid as a single premium, it can’t be considered for 80C tax deduction

* The current regulation makes it mandatory for the minimum cover to be to be 110% of the premium for people less than 45 years old.

This means that if I paid a single premium of 1L, the cover should be at least 1.1L

* As per Section 10 (10D(c)), the premium should not exceed 20% of the cover in any year of the policy’s tenure. Only then is the entire amount tax-free at maturity. If not, the maturity is added to the income of that year and taxed.

This means that if my cover is 1L, then premium should not exceed 20000 in any given year for the duration of the policy

Points to note:

* The sub section 3 of Section 80 C of the Income Tax Act 1961 clearly points out that a deduction is available only to so much of the premium, which is not in excess of the 20% of the sum assured [the technical term for the amount of life cover the individual taking the policy opts for] on the policy.

It means: If the sum assured is 3 Lakh, 20% of 3 Lakh = 60000. If any amount greater than 60000 is paid as a single premium, it can’t be considered for 80C tax deduction

* The current regulation makes it mandatory for the minimum cover to be to be 110% of the premium for people less than 45 years old.

This means that if I paid a single premium of 1L, the cover should be at least 1.1L

* As per Section 10 (10D(c)), the premium should not exceed 20% of the cover in any year of the policy’s tenure. Only then is the entire amount tax-free at maturity. If not, the maturity is added to the income of that year and taxed.

This means that if my cover is 1L, then premium should not exceed 20000 in any given year for the duration of the policy

Investment outside india

Source: "A Google in your portfolio"; ET Wealth; Dec 27,2010

Taxation angle :

Taxation angle :

This is a major disadvantage global investors have to bear with. While long-term capital gains from equities listed in India are tax free, they are taxable for foreign stocks. So be prepared to dole out long-term capital gains tax at 20%, but only after indexation to factor in inflation

For the passive investor:

Not comfortable venturing out? There are several global diversification options available for you here as well. The first option is India depository receipts (IDRs) of global stocks listed in India. Standard Chartered Bank (SCB) IDR, the only option available at present, offers good value

Taxation :

There is no confusion with regard to taxation here. It will be treated as debt scheme. So investors have to hold on for a year to take the benefit of long-term capital gains tax. Another option is to use the domestic mutual funds that invest a small portion of their corpus in international markets like Templeton India Equity Income Fund

Taxation angle : This is a major disadvantage global investors have to bear with. While long-term capital gains from equities listed in India are tax free, they are taxable for foreign stocks. So be prepared to dole out long-term capital gains tax at 20%, but only after indexation to factor in inflation

For the passive investor:

Not comfortable venturing out? There are several global diversification options available for you here as well. The first option is India depository receipts (IDRs) of global stocks listed in India. Standard Chartered Bank (SCB) IDR, the only option available at present, offers good value

Taxation :

There is no confusion with regard to taxation here. It will be treated as debt scheme. So investors have to hold on for a year to take the benefit of long-term capital gains tax. Another option is to use the domestic mutual funds that invest a small portion of their corpus in international markets like Templeton India Equity Income Fund

Monday, 17 January 2011

How to get most out of jewellery sale?

Source: ET Wealth ,10Jan2011

· Only a gram of jewellery with 91.6% of gold passes muster as 22 carat gold. It means 91.6% gold purity or 916 points of gold is present in every 1000 points of the item. 1000 is 24 carats, 750 is 18 carats.

· Retaining a record of purchase while buying or selling jewellery

· For investment, turn to gold bars or coins

Testing purity

· Jewellers test using a Caratometer. This is a faulty practice.

· A person selling or buying gold can demand fire assay testing for a nominal fee (also called hallmarking). A part of the gold is melted and tested. The marking is done using punches or a laser marking machine. The Bureau of Indian Standards (BIS) website lists labs that provide hallmarking.

· You can also demand a hallmark certificate from the jeweler. The cost varies and is usually around Rs. 25 a unit.

· Hallmark has long been used as a safeguard to buyers of gold and gold articles in many countries.

· It jewellery is hallmarked, the mark on the jewellery is more authentic than paper (certificate) as the paper may relate to any other jewellery.

Rates

· Checking rates – SMS “GOLDRATE” on 575758 (All India Gems and Jewellery Trade Federation (AIGJF) for the day’s gold rate. (http://www.gjf.in/). Please note that "GOLDRATE" is one word. If you send an SMS to "GOLD RATE", then many jewellers would have registered and the service will pick up the first one and send you details of the schemes of that jeweller.

· If the message says, “22K S:2033, 22K B:1911”, a jeweler will sell 22 carat jewellery @ 2033 and will buy back @ 1911.

Thursday, 13 January 2011

Access your credit information report - India

Source - ET Wealth-3 jan 2011

Your Credit Information Report (CIR) contains details of our credit history and track record in taking and repaying loans from banks and finance companies. A loan applicant with a good credit record will find access to loans easier, faster and on favourable terms.

The credit information bureau of India Ltd (Cibil) consolidates the information on individual borrower's credit history, sourced from different member credit institutions such as banks, credit card companies and NBFCs, into a single report called the CIR. This is then made available to its members (banks, finance companies) to facilitate their lending decisions.

You can access your own CIR for a fee. You can also check and correct errors in the report and to initiate action to improve your credit record. It is a good idea to keep your CIR updated and correct, so it is easier and faster for you to apply and get loans at competitive rates

How do I get my CIR?

1. Fill up a CIR request form. It can be downloaded from www.cibil.com/accesscredit.htm

2. Submit self-attested copies of address proof (bank statement, utility bill) and identity proof (PAN card, passport or voter's ID)

3. Make a demand draft for Rs. 142 in favor of Credit Information Bureau (India) Ltd., payable at Mumbai. If paid online, send unique registration ID and transaction ID.

4. Send documents and draft to Cibil at : Hoechst House, 6th Floor, 193 Backbay Reclamation, Nariman Point, Mumbai 400021

Points to Note:

Restricted Access: Your CIR is accessible only to you and to members of Cibil who may want to cross check the credentials of a prospective borrower. A third person can't see your CIR

Corrections: If you find errors in your CIR, you have to approach your lender. Cibil will alter the CIR only when members report changes

Rating: CIR only provides factual information on your repayment record. It does not classify, rank or rate you based on your credit history.

Tuesday, 11 January 2011

Tax: 5 reasons why insurance won't save tax

1. No deduction: Under DTC, an insurance policy that offers a cover of less than 20 times the annual premium won't be eligible for tax deduction.

2. Tax on maturity: If the 20 times life cover condition is not met, even the income accruing from the policy will be taxable

3. Lower limit: The tax deduction limit for life insurance will be reduced from the present 1L to 50000 per year. The 50000 limit would also include the amount paid for tuition fees of children as well as medical insurance

4. Tax on withdrawals: Partial withdrawals from an insurance plan before maturity will be taxable under DTC

5. Tax on surrendering: The surrender value of a plan will also be taxable.

6. ULIPs has a lock-in period of 3 years. This has been extended to 5 years now by IRDA.

MF: Updating address in fund investments

If an investor has changed his house and wants to update the new address in his mutual fund details, he will have to write to each fund house that he has invested in. Instead, if he just updates his address with a central agency named CDSL Ventures Ltd (CVL), all his folios across funds would get updated. CVL is also responsible for processing the KYC. CVL updates the address of the investor and the same gets communicated to all the investment houses. The process of address change takes around 10 days.

Steps:

1. Fill up the form and submit documents for verification to the designated point of service (POS). Forms can be downloaded from http://cvlindia.com/include/pdf/individual.pdf

2. The POS will give an acknowledgement. A copy of this has to be enclosed with mutual fund purchase documents.

3. If you want to change the address and also apply for redemption, give at least 10 days for the update before redemption

4. KYC is mandatory for all joint holders but address in a folio is only of the first holder. No need to make changes for all the holders.

Points to note:

KYC first: Investors have to be KYC compliant first before updating their address details:

CVL is the only route: Fund houses and registrars will not accept change of address requests from investors. this is done only through CVL

PAN: Your PAN is used to identify all the folios held by you across funds. Quoting the correct PAN enables updating the records correctly.

NRI: Those who provide overseas address will have to get it verified by their bank or consulate.

Why are research reports - stocks free?

In India, research reports are free, so research in effect is a cost centre

The positives:

* Analysts find undervalued stocks and recommend these stocks to existing and prospective clients who can profit from this.

* brokers who cover institutional clients will cover large caps

The not so positives:

* The prime objective of a research report is to induce a transaction. It allows the sales force to go out into the market, sell stocks and generate commissions. Every transaction brings in broking income

* It is essential to bring out a "buy" report. This will help target new and existing clients. A sell report will impact only those clients who hold that stock. By perception, people rather buy low and sell high. Not many people involve in short selling.

* At times, the owner of a broking firm or the portfolio of a broking firm might have a stock that is not doing well. It might then release a Buy report which might cause interest in the market and thus help increase its price.

Solutions:

* An investor should be able to differentiate reports based on which broking house is originating the report

* There is a disclosure section, large brokerages state whether they own the stock or a sister firm of the brokerage has an investment banking relationship with the company. This is something a retail investor should look for.

Monday, 10 January 2011

Bidding for a house

Source: ET Wealth-10Jan 2011

Auction Facts

why?

Property cheaper by 15-20% than market price

How?

* Banks advertise in local dailies with property details, date and place of auction

* Bidders can visit the property

* Submit expression of interest by specified date

* Submit earnest money

* Attend the auction

* Banks also give home loans for auctioned property

Watch Out

* Bank may ask for part of reserve value immediately after the bid

* Buyer has to bear all outstanding dues on the property

Further,

1. Buyer should check important documents such as possession record in title before bidding. The title of the property can be verified at registry offices.

2. An investor should also verify municipal records to find out whether any tax is outstanding

3. An investor should check with the society for any outstanding maintenance or electricity dues.

Auction Facts

why?

Property cheaper by 15-20% than market price

How?

* Banks advertise in local dailies with property details, date and place of auction

* Bidders can visit the property

* Submit expression of interest by specified date

* Submit earnest money

* Attend the auction

* Banks also give home loans for auctioned property

Watch Out

* Bank may ask for part of reserve value immediately after the bid

* Buyer has to bear all outstanding dues on the property

Further,

1. Buyer should check important documents such as possession record in title before bidding. The title of the property can be verified at registry offices.

2. An investor should also verify municipal records to find out whether any tax is outstanding

3. An investor should check with the society for any outstanding maintenance or electricity dues.

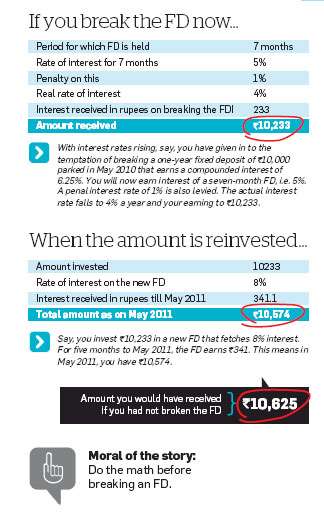

When to Break an FD

Source: ET-Wealth-10Jan2011

* There is a reduced interest to 5% in the example.

* Over an above that there is a 1% penalty. This is confusing.

* Over an above that there is a 1% penalty. This is confusing.

Gratuity

Source: ET Wealth-10Jan2011

* Gratuity is a lump sum amount paid to an employee on retirement. Companies use it as a retention tool.

* You get gratuity if you have completed five years in a company. There is a cap of 10lakh

* Gratuity calculator:

(Your last drawn monthly salary(basic + DA) /26)*15*X=Gratuity

26=1 month

15=15 days of service in a year provided as DA

X = No of years worked

* If you completed 7 years of service and your last drawn salary was 45K per month, then gratuity = 1.8L

* This is mandatory for companies with more than 10 employees on their payrolls to give gratuity to employee on resignation, retirement and termination of service

* Condition of 5 years of service is relaxed in case of death or permanent disablement of the employee.

* Tax exemption has been raised to 10lakh.

* Gratuity is a lump sum amount paid to an employee on retirement. Companies use it as a retention tool.

* You get gratuity if you have completed five years in a company. There is a cap of 10lakh

* Gratuity calculator:

(Your last drawn monthly salary(basic + DA) /26)*15*X=Gratuity

26=1 month

15=15 days of service in a year provided as DA

X = No of years worked

* If you completed 7 years of service and your last drawn salary was 45K per month, then gratuity = 1.8L

* This is mandatory for companies with more than 10 employees on their payrolls to give gratuity to employee on resignation, retirement and termination of service

* Condition of 5 years of service is relaxed in case of death or permanent disablement of the employee.

* Tax exemption has been raised to 10lakh.

Friday, 7 January 2011

Tax:Education loan to lower tax

Source: ET-Wealth-3Jan2011: 8 Tax Saving Secrets

Use education loan to lower tax

The rising cost of higher education is forcing people to borrow money to pay the fee of their children’s professional courses. The taxman is sympathetic and offers a deduction that can lower the cost of the loan. The interest paid on an education loan is fully deductible from taxable income under Section 80E. Till a few years back, this deduction was available only to the borrower. Now, even a parent or a spouse can avail of it. What’s more, this now includes loans taken for vocational courses. “If a parent or legal guardian takes the loan, he can claim deduction for the interest paid for up to eight successive years, starting from the year in which the interest is first paid,” says Shanbhag.

However, loans taken for siblings and other relatives do not qualify. Also, the lender must be a recognised financial institution; loans from employers or individuals do not count.

How much tax can you save: If you take a Rs 10 lakh education loan at 10% interest for 8 years, you can save Rs 1.41 lakh in tax in the highest tax bracket. This will bring down the effective cost of the loan to 7% per annum.

Proof required: Loan statement from lender.

Highlights - Ajay

* Even a parent or a spouse can avail of it

* Loan can be taken for vocational courses as well

Tax: Claim benefits for your political affiliations

Source: ET-Wealth-3Jan2011

Article: 8 Tax Saving Secrets

Claim benefits for your political affiliations

Can you lower your tax if you have political connections? Apparently you can. Any amount contributed to a recognized political party can be claimed as a deduction under Section 80GGC (80GGB for corporates). “This is a new deduction and was introduced in April 2010. The donation can also be made to the electoral trust which works for the purpose of conducting elections,” says Sheth. Interestingly, unlike other deductions, there is no ceiling on the amount that can be claimed as a deduction. Of course, the deduction is available only if the donation went into the party coffers.

Cash given to individuals doesn’t count. Other donations also get you tax benefits. Under Section 80G, donations to charitable organizations get deduction ranging from 50% to 100%. It’s a good idea to know how much deduction would be available before you write a cheque. However, There is a ceiling to the deduction a taxpayer can claim in a year. “The quantum of deduction is limited to 10% of the gross total income of the donor,” says Tapati Ghose, partner at Deloitte Haskins & Sells. Also, only cash donations are taken into account. Food, clothes and medicines do not qualify.

How much tax can you save: In the highest tax bracket, a donation of Rs 1 lakh to a political party can bring down your tax by Rs 30,900.

Proof required: You must have a stamped receipt of the payment from the political party.

Highlights - Ajay

* Under Section 80G, donations to charitable organizations get deduction ranging from 50% to 100%

* The quantum of deduction is limited to 10% of the gross total income of the donor

Term Insurance - Claim Rejection Ratio

Claim rejection ratio for LIC is around 1%. For private players, claim rejection is in the region of 20-25%

Silver

How can you buy e-silver?

You need to have a trading account with any of the 370 odd brokers registered with the National Spot Exchange. You also need a demat account, which is different from the demat account needed for shares and securities.

How much will it cost?

Paper work will cost about Rs.150 and annual charges for maintaining the demat account are Rs 400-700

What is the smallest unit that one can buy?

One unit of e-silver equals 100g. That would cost you about Rs.4500 at current prices

Can I take physical delivery of silver?

You can hold the units in either electronic form or opt for physical delivery. You can make a request for a physical delivery to your depository participant.

What is the cost of physical delivery?

Taking physical delivery involves fixed charges, so it isn't worthwhile to take delivery of small quantities. You have to pay VAT of 1% anywhere in the country and delivery charge of Rs. 200 for every instruction that you make for delivery.

Where can I take physical delivery?

Currently you can take delivery in Mumbai, Ahmedabad and Delhi

EPF - tips

Transfer, don't withdraw

You need to fill a "Form13" and deposit it with the EPFO. The form you are required to fill has details of your previous organization including the previous EPF number and the regional providend fund office.

What if you don't transfer?

The balance was earning interest till the time of withdrawal. This will stop from April 2011

Tax: Pay lower tax if someone is ill

Source: ET-Wealth-3Jan2011

Article: 8 Tax Saving Secrets

Pay lower tax if someone is ill

The treatment of a chronic illness can be a drain on the finances of a taxpayer. That’s why the Income tax Act allows a taxpayer to claim a deduction of Rs 40,000 if he has a dependent who suffers from any of the ailments specified under Section 80DDB. “The deduction is higher at Rs 60,000 if the patient is a senior citizen,” says chartered accountant Paras Savla. The diseases include, neurological diseases (including dementia, dystonia musculorum deformans, motor neuron disease, ataxia, chorea, hemiballismus, aphasia and Parkinson’s disease), malignant cancers, full-blown AIDS, chronic kidney failure and haematological disorders (haemophilia and thalassaemia). Dependents can include spouse, children, parents and siblings. However, there are a few conditions.

The patient should be wholly or mainly dependent on the taxpayer and should not have separately claimed deduction for the disability. If the amount spent is reimbursed by the employer or an insurance company, there is no deduction. If the taxpayer gets a partial reimbursement of the expenses, the balance can be claimed as deduction.

How much tax can you save: If a dependent is a patient, the taxpayer’s liability comes down by 12,360 in the highest income bracket. If the patient is a senior citizen, the tax is lower by Rs 18,540.

Proof required: One needs a certificate of the illness from a specialist in a government hospital.

Highlights - Ajay

* Dependents can include spouse, children, parents and siblings. However, there are a few conditions

* If the amount spent is reimbursed by the employer or an insurance company, there is no deduction. If the taxpayer gets a partial reimbursement of the expenses, the balance can be claimed as deduction.

Tax: Get deduction for rent even without HRA

Source: ET-Wealth-3Jan2011: 8 Tax Saving Secrets

Get deduction for rent even without HRA

House rent can account for as much as 40-50% of the total household expense. That’s why the house rent allowance is exempt from tax to a certain limit. But what if your salary does not include an HRA component or you are a self-employed professional or businessman? Under Section 80GG, you can claim deduction of the rent paid even if you don’t get HRA. “Not many people are aware of this deduction,” says chartered accountant Mehul Sheth. But there are stiff conditions to be met. The least of the following three can be claimed as deduction: rent paid less 10% of total income; or Rs 2,000 a month; or 25% of total income. Also, the taxpayer should not be drawing any HRA or any housing benefit.

Besides, he or his spouse or minor child should not own a house in the city where he stays and he should not be claiming tax benefits for some other self-occupied house. Whew. Incidentally, if you are living in your parents’ house, you can pay rent to them. If your parent has no other income or pays a lower tax, this can bring down your tax liability significantly. However, the rent will be taxable as the income of the parent after a 30% standard deduction. This means, you can pay a senior citizen parent up to Rs 3.43 lakh a year.

How much tax can you save: Given the stiff conditions, one can’t claim more than Rs 2,000 as deduction per month under Sec 80GG. But this can bring down your tax by Rs 7,400 a year in the highest tax bracket.

Proof required: Taxpayer has to submit a declaration on form 10-BA that he is paying rent and not receiving HRA.

Tax:Use losses in stocks to cut tax

Source: ET-Wealth-3Jan2011: 8 Tax Saving Secrets

Use losses in stocks to cut tax

Can you gain from the short-term losses you made on stocks? Yes, says the Income Tax Act. If you have made any long-term capital gains from sale of property, gold or debt funds, you can set them off against short-term capital losses made on stocks and bring down your tax liability. “Short term capital losses can be set off against both short-term capital gains as well as taxable long-term capital gains,” says Sandeep Shanbhag, director of Wonderland Consultants, a Mumbai-based tax planning and financial consultancy. This can be especially useful for someone who has booked profits on gold ETFs and physical gold this year. Suppose you have sold a property and made a long-term capital gain of Rs 30 lakh after indexation.

At 20%, the tax payable on this long-term capital gain is Rs 6 lakh. However, if you have also sold some junk stocks during the year and made a short-term loss of Rs 3 lakh, you can set this off against the gains from the property. Then the gain from the property will get reduced to only Rs 27 lakh and the tax payable will be Rs 5.4 lakh. However, the law makes a distinction here. One cannot set off short-term gains from stocks against long-term capital losses from the other assets. “Long term capital losses can only be set off against taxable long-term capital gains,” says Shanbhag.

How much tax can you save: Setting off a short-term loss of Rs 3 lakh against long-term gains can help you save Rs 60,000.

Proof required: Keep record of your equity trading account statement with details of the transactions that resulted in losses.

Highlights - Ajay

Short Term Capital Losses <-> STCGains

STCL <-> Taxable LTCG

STCG can't be offset against LTCL

LTCL <-> Taxable LTCG

Subscribe to:

Comments (Atom)